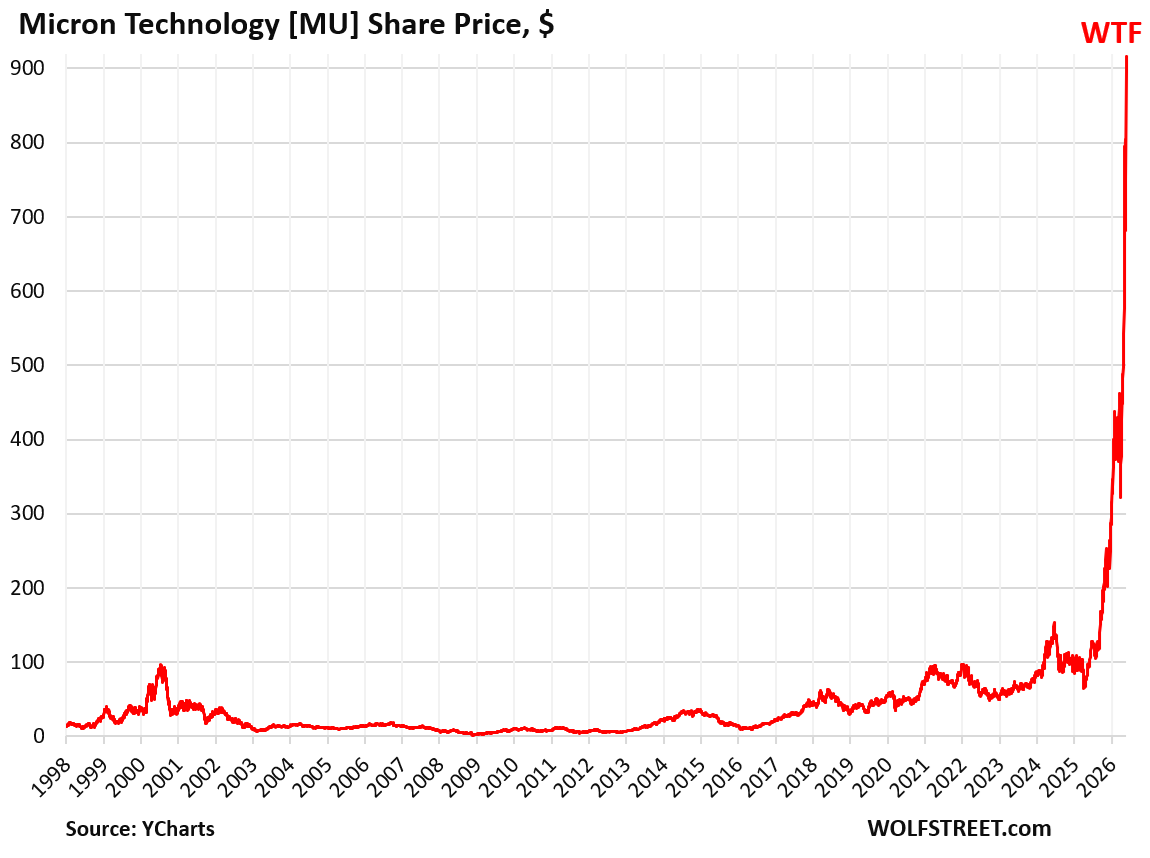

Micron Technology has a nasty habit of crushing its shareholders. The memory chip maker's stock has crashed by 50% to 98% after every major spike since the dot-com bubble. Now, with AI mania pushing shares to all-time highs, investors are betting this time is different. History suggests otherwise.

The Big Picture

Micron isn't just any chip company. It's one of only three global manufacturers of DRAM and NAND memory, the essential components inside every smartphone, laptop, and AI server. When demand surges, Micron flies. When supply catches up, it plummets. This cycle has been merciless since the company went public in 1984.

The pattern is stark. During the dot-com bubble, the stock hit roughly $100 (split-adjusted). It then collapsed to under $2 by 2003 — a 98% loss. It surged to $70 in 2007, only to crash to $2 again in 2009. In 2018, it reached $60; by 2020, it was $30. Each time, the decline was at least 50%. Most recently, it hit $100 in 2021 and fell to $50 in 2023. Now, fueled by AI chip demand, it's above $150. How far will it fall this time?

“Micron's pattern is so consistent it should be a warning: every peak has been followed by a decline of at least 50%.”

By the Numbers

- Historical minimum decline: Every cycle has seen a drop of at least 50%, with the worst reaching 98%.

- Dot-com bubble peak: Stock reached ~$100 in 2000, then fell to under $2.

- 2018 peak: $60; 2020 trough: $30.

- 2021 peak: $100; 2023 trough: $50.

- Current price (May 2026): Over $150, driven by AI demand.

Why It Matters

The problem isn't Micron as a business. The company is solid, with revenues exceeding $20 billion. The problem is valuation. Investors have priced in growth that may not materialize at the expected pace. AI chip demand is real, but supply is also ramping up. Samsung, SK Hynix, and Micron are pouring billions into new capacity. When that capacity hits the market, memory prices will fall. It's the semiconductor curse: there's always an oversupply at the end of the cycle.

The winners here are chip buyers — big tech firms like Amazon, Google, and Microsoft — who benefit from lower prices. The losers are investors buying at the top. Micron's pattern suggests the stock could fall to $75 or less within two years. That would be a 50% decline from current levels.

What This Means For You

If you're an investor, this is a playbook of what not to do. Buying Micron at its all-time high has been, repeatedly, a recipe for losses. The AI narrative is compelling, but the semiconductor cycle is relentless.

- 1Don't buy at the peak: Wait for a 40%+ decline from the high before considering an entry. History shows there's always a cheaper buying opportunity.

- 2Diversify away from cyclical semiconductors: If you have tech exposure, ensure it's not concentrated in companies like Micron, whose revenues depend on a boom-bust cycle.

- 3Use options to hedge: If you already own shares, buying 12-month puts can be a cheap way to insure against a 50% drop.

What To Watch Next

Micron's next earnings reports will be critical. If the company announces slowing revenue growth or rising inventories, it could signal the cycle is turning. Also watch capital expenditure decisions from Samsung and SK Hynix. If they boost output, memory prices will fall.

U.S.-China trade policy is another wild card. Any restrictions on chip sales to Chinese firms would reduce demand and accelerate the downturn.

The Bottom Line

Micron is a case study in how enthusiasm for a transformative technology can lead to unsustainable valuations. AI is real, but the semiconductor cycle hasn't been repealed. Investors would do well to remember history: every peak is followed by a valley. And for Micron, that valley is often deep. Prepare for the next crash.

Deeper Analysis: Macro Context and Investor Implications

To gauge the magnitude of risk, it's useful to compare the current situation with past cycles. In 2000, Micron's price-to-earnings ratio (P/E) reached astronomical levels, exceeding 100x. In 2018, the P/E hit 15x, yet the subsequent decline was equally severe. Today, with a P/E of roughly 25x based on 2026 earnings estimates, the stock isn't as overvalued as in 2000, but the supply-demand cycle is faster than ever. DRAM production capacity doubles every two years, and current investments by Samsung and SK Hynix could create an oversupply by 2027.

Moreover, the AI market is concentrated among a few buyers: the hyperscalers. If they reduce spending on AI servers, memory demand could drop sharply. There are already signs of a slowdown: Meta and Google have moderated their capital expenditure projections for 2026. A 10% cut in AI server demand could translate into a 20% drop in Micron's revenue, given its operating leverage.

For the retail investor, the lesson is clear: don't get caught up in the hype. Micron's history is not just a warning; it's a textbook case of market behavior. Those who bought at the 2000 peak took 17 years to recover their investment (inflation-adjusted). In 2018, the recovery took 4 years. This time, with higher valuations and a faster cycle, the wait could be just as long.

Near-Term Catalysts

The coming months will be decisive. Micron's fiscal third-quarter earnings report (June 2026) could show revenue growth slowing from 50% year-over-year to 30%. If guidance is weak, the stock could drop 20% in a single day. Additionally, the Biden administration's decision on tariffs for Chinese chips could impact Micron, which gets 15% of its revenue from China. Any additional restrictions would be a severe blow.

In short, the time to sell may be now. Investors holding positions should consider reducing exposure or buying protection. History doesn't lie: after every peak, Micron falls. And this time, the fall could be especially painful because the market has priced in growth that may never arrive.