Inflation is the bane of the bond market. And it is now demanding multiple rate hikes, starting late this year.

The Big Picture

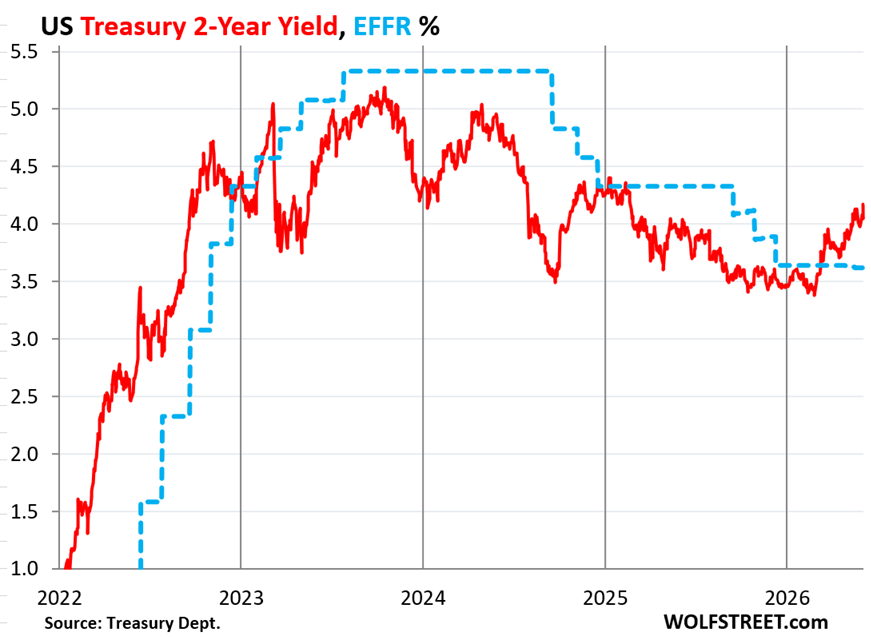

The Treasury market is sending a clear signal: inflation is not transitory, and the Federal Reserve will have to act. Yields on U.S. government bonds have surged in recent weeks as traders price in a higher probability of rate hikes beginning as soon as October 2026. The 10-year yield breached 4.8% on June 5, its highest level since May 2025, and the 2-year yield climbed above 5%, steepening the curve.

This is not a minor technical adjustment. It represents a regime change. For months, investors bet that inflation would moderate without aggressive Fed action. That bet is unraveling. Consumer and producer price data continue to surprise to the upside, while a tight labor market keeps wage pressures elevated. The May CPI rose 0.4% month-over-month, double the consensus estimate, while core inflation held at 3.1% year-over-year. The labor market added 272,000 jobs in May, well above the 185,000 expected, and the unemployment rate fell to 3.7%. These data points have triggered a repricing in fed funds futures, which now imply a greater than 60% probability of a rate hike at the September FOMC meeting, and at least three quarter-point increases by year-end.

“The market now expects at least three quarter-point rate hikes by year-end 2026.”

By the Numbers

- Expected rate hikes: At least three 25-basis-point increases priced in starting October 2026, with a cumulative probability of 75% for December.

- 10-year Treasury yield: Surged past 4.8%, the highest level in over a year, and the curve has partially disinverted.

- Core inflation: Remains above 3%, well above the Fed's 2% target, with May data showing an unexpected uptick in services and shelter.

- September hike probability: Fed funds futures show over 60% chance of a move, up from 30% a month ago.

- Breakeven inflation rate: The 10-year breakeven has widened to 2.6%, signaling higher long-term inflation expectations.

- Bond market volatility: The MOVE index, measuring implied volatility, has risen 15% in the past month, reflecting uncertainty.

- TIPS yields: The 10-year TIPS real yield stands at 1.8%, the highest since 2009, offering attractive real returns.

Why It Matters

This changes the calculus for every bond investor. Long-duration Treasuries, once considered safe havens, are suffering capital losses. Anyone who bought 10-year notes when yields were at 4% is now sitting on negative real returns after accounting for inflation. For instance, a 10-year bond issued a year ago with a 4% coupon has lost approximately 7% of its market value. Bond funds with average durations of 6-8 years have posted negative returns in the second quarter, and outflows have accelerated.

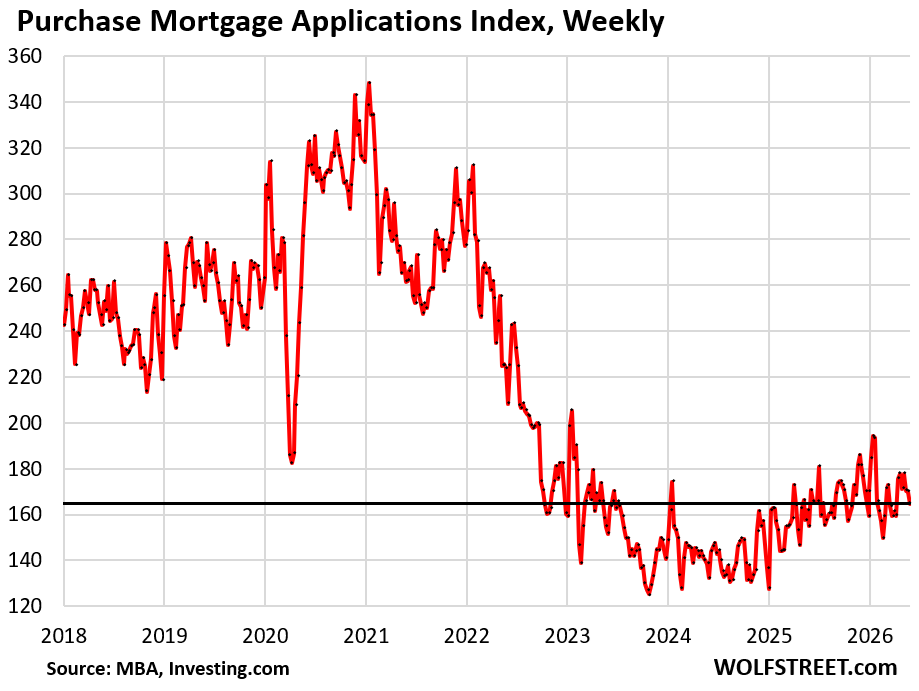

The winners could be short-duration bonds and Treasury Inflation-Protected Securities (TIPS). Banks may also benefit from wider net interest margins. But for the broader economy, higher rates mean tighter financial conditions, which could slow business investment and consumer spending, particularly in housing and autos. Mortgage rates have already risen above 7%, and mortgage applications have fallen 12% over the past four weeks. Highly leveraged companies face higher refinancing costs, which could increase default rates.

The Fed faces a dilemma: raise rates and risk a recession, or hold steady and risk entrenched inflation. The market is forcing the issue, and the central bank's credibility is on the line. Cleveland Fed President Loretta Mester has stated, "If inflation does not show sustained progress toward 2%, I will be in favor of raising rates in September." Other FOMC members, like Christopher Waller, have adopted a more hawkish tone, indicating that "the tight labor market and persistent inflation justify preemptive action."

What This Means For You

If you hold bonds, it's time to rethink duration. Long-dated Treasuries are vulnerable if the Fed follows through on rate hikes. Consider shifting to shorter maturities or inflation-linked securities. For institutional investors like pension funds, the rise in yields offers opportunities to improve long-term returns, but requires active duration risk management.

- 1Review your bond portfolio: Reduce exposure to long-term bonds and increase allocation to short-term debt (under 2 years). The 2-year Treasury now yields above 5%, offering attractive returns with low volatility.

- 2Consider TIPS: Inflation-protected bonds offer a hedge and are becoming more attractive. The 10-year TIPS real yield of 1.8% is the highest since 2009, providing solid real returns.

- 3Diversify into alternatives: Gold, commodities, and value stocks may outperform in a rising-rate environment. Gold is up 12% year-to-date, and the S&P GSCI commodity index has gained 8%.

- 4Explore carry trades: In currencies, the dollar has strengthened 5% against the euro in the past month, and investors can exploit interest rate differentials with long USD positions.

What To Watch Next

The key date is the Fed's July meeting. If June inflation data doesn't show clear moderation, the Fed will likely prepare markets for a September hike. Watch for hawkish commentary from Fed officials, especially Chair Powell. His speech at the Jackson Hole Symposium in late August will be crucial for signaling policy direction.

Also monitor the labor market. If employment remains strong, the Fed has room to hike. But if cracks appear, the dilemma intensifies. The June payrolls report, due July 2, will be a key data point. Additionally, watch services inflation, which has shown troubling stickiness, and housing prices, which continue to rise at a 5% annual rate.

On the fiscal side, the Treasury will issue $1.2 trillion in new debt in the second half of the year, which could add upward pressure on yields. The combination of a hawkish Fed and heavy supply may keep yields elevated for months.

The Bottom Line

Inflation is forcing the bond market to price in a tightening cycle that seemed unlikely just months ago. Investors must prepare for higher rates for longer. Those who don't adjust risk significant losses in the months ahead. Patience with inflation has run out.

The market is speaking, and the Fed is listening. The question is whether it can act without breaking the economy. For investors, the key is active duration risk management and seeking real protection. The coming months will be decisive in determining whether the Fed can achieve a soft landing or whether the economy is headed for a policy-induced recession.