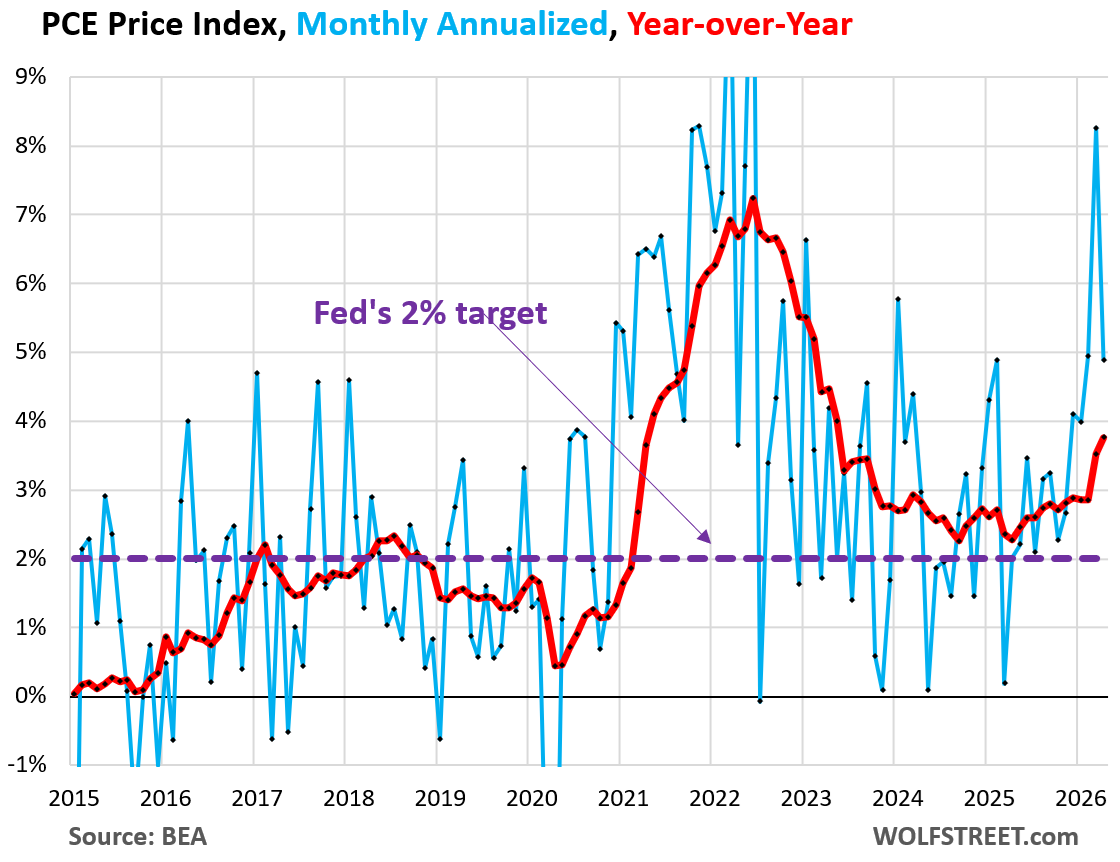

April's Personal Consumption Expenditures (PCE) price index surged to 4.2% year-over-year, nearly double the Federal Reserve's 2% target. The trend reversal began a year ago, and now services inflation remains stubbornly high while goods prices—from food to computers to gold jewelry—are accelerating again. This data, released May 29, 2026, confirms the Fed is losing its grip on inflation.

The Big Picture

The disinflation trend reversed in May 2025, exactly one year ago. Since then, services inflation has been stuck at elevated levels, with no sign of easing. Now, goods inflation is also picking up, driven by the AI boom that has boosted demand for computers and software, and by the surge in gold prices that has lifted jewelry costs.

Core PCE, which excludes food and energy, also beat expectations, coming in at 3.8% year-over-year. The Fed had projected inflation would return to its target by end of 2026, but this data suggests a longer, more painful path. Financial markets reacted with bond and stock declines, pricing in higher-for-longer rates.

“The April PCE inflation data confirms the Fed is losing control over prices, with inflation nearly double its target.”

By the Numbers

- Headline PCE inflation: 4.2% year-over-year in April, up from 3.6% in March.

- Core PCE inflation: 3.8% year-over-year, up from 3.4% previously.

- Services inflation: Stuck above 5% annually for the past year.

- Goods inflation: Rebounded to 3.1% annually, driven by computers (+8.2%) and gold jewelry (+12.5%).

- Fed target: 2% annually, still far off.

Why It Matters

This data is a major setback for the Fed. The narrative that inflation was 'transitory' or only affected volatile goods has collapsed. Services inflation, which is more persistent because it includes rents and wages, is not budging. And now, the AI boom is creating a new inflationary wave in technology, as companies compete for chips, servers, and software, driving up costs.

Winners in this environment are real assets: gold, inflation-indexed real estate, and commodities. Losers: long-duration bonds, high-valuation growth stocks, and fixed-income consumers. The Fed faces a dilemma: raise rates further and risk a recession, or accept higher inflation for longer.

What This Means For You

For investors, it's time to review portfolios. Persistent inflation erodes the purchasing power of bonds and stocks of companies with thin margins. Seek assets that benefit from inflation, such as commercial real estate REITs with indexed leases, technology infrastructure companies (semiconductors, data centers), and commodities like gold.

For homebuyers, mortgage rates will stay high. The Fed won't cut rates soon, so 30-year fixed mortgages will likely remain above 7%. If you're considering buying, look into adjustable-rate mortgages (ARMs) with lower initial rates, but be prepared for potential increases.

- 1Review your portfolio: Reduce exposure to long bonds and high-growth stocks. Increase allocation to real assets and companies with pricing power.

- 2Lock in mortgage rates: If planning to buy, consider a fixed-rate mortgage now before rates rise further.

- 3Protect your savings: Seek high-yield savings accounts or inflation-indexed bonds (TIPS) to preserve purchasing power.

What To Watch Next

The next key data point will be the May Consumer Price Index (CPI), due June 12. If it shows a similar acceleration, the Fed may be forced to raise rates at its July meeting. Also watch the minutes of the Fed's May meeting, due next week, for any hawkish signals from FOMC members.

Additionally, the AI boom will continue to pressure semiconductor and software prices. Companies like Nvidia, AMD, and Microsoft are investing billions in infrastructure, and those costs will be passed to consumers. The question is whether AI demand is strong enough to sustain these prices or if it's a bubble.

The Bottom Line

April's PCE inflation is a wake-up call. The Fed is running out of options: raising rates could crush the economy, but not doing so means accepting structurally higher inflation. For investors, the key is to adapt to a 'higher-for-longer' rate environment and seek inflation-protecting assets. The bond market is already pricing in fewer rate cuts, and equities may face more volatility. Stay diversified and avoid overconfidence in long-duration assets.

2026 may be remembered as the year the Fed lost control of inflation—or the year it finally tamed it. For now, bets are on the former.

Context and Near-Term Catalysts

April's data is not an isolated event. Services inflation has been above 5% for over a year, and the recent acceleration in goods suggests pressures are broadening. The Fed had hoped that moderation in rents and wages would help, but April data showed owners' equivalent rent (OER) rose 0.5% month-over-month, the largest gain in six months. This points to a still-tight housing market with limited supply and sustained demand.

On the tech front, spending on data centers has surged. Industry estimates put AI infrastructure investment at $200 billion in 2026, up 40% from last year. This is driving up semiconductor prices, which rose 8.2% annually in April. Companies like Nvidia and AMD are seeing record margins, but costs are passed to consumers through higher software and cloud service prices.

Upcoming catalysts include the G7 meeting in June, where trade and tech policies could affect semiconductor supply chains. Also, OPEC+ meets on June 1 to decide on production quotas; an additional cut would be bad news for inflation.

Implications for Investors and Traders

For fixed-income investors, the message is clear: 10-year Treasury yields could exceed 5% if inflation doesn't ease. The yield curve is flattening, with the 2-10 year spread narrowing to 20 basis points, indicating expectations of an economic slowdown but persistent inflation. TIPS offer direct protection, with real yields still positive.

In equities, sectors like consumer tech and discretionary could suffer if rates rise further. In contrast, tech infrastructure companies (semiconductors, data centers, network equipment makers) benefit from AI spending regardless of rates. Energy and basic materials companies also stand out, benefiting from commodity inflation.

A practical tip for traders: consider options strategies to hedge against volatility. For example, buying puts on SPY or QQQ can be cheap insurance if markets correct. You can also sell covered calls on overvalued growth stocks to generate income while waiting.

Long-Term Outlook

The base case is that the Fed holds rates steady through end-2026, with a possible cut in 2027 if inflation eases. But the risk is that inflation stabilizes around 3-4%, forcing the Fed to hike again. That would be a blow to markets, which already price in two cuts in 2026.

On the positive side, AI innovation could boost productivity long-term, helping contain inflation. But that effect will take years to materialize. Meanwhile, the global economy faces headwinds: a slowdown in China, trade tensions, and a still-tight US labor market with unemployment at 3.9%.

In summary, April 2026 marks a turning point. The Fed can no longer ignore services inflation or the AI impact. Investors must prepare for a high-rate, volatile environment, with opportunities in real assets and companies with pricing power. Patience and diversification are key.