Nearly 4 in 5 Americans don't feel their financial future is secure. A new study from Intuit Credit Karma and Harris Poll suggests homeownership could be the fix—but high prices and rates make it a tough sell.

The Big Picture

A staggering 78% of Americans lack confidence in their financial future, according to a new Intuit Credit Karma/Harris Poll study. Even among those who have saved and played by the rules, the anxiety persists. Nearly three-quarters (72%) say they'll never have enough money to achieve the American dream. This distrust is not new, but it has intensified in recent months due to a combination of macroeconomic and geopolitical factors.

The economic backdrop is grim. President Trump's economic approval rating slumped to 30% in April, per an AP-NORC survey—down 8 points from March and 9 points since the Iran war began in February. The conflict pushed gas above $4 a gallon in late March, raising costs for everything from commuting to home heating. Inflation hovers around 3%, eating into wages. Adding to this is uncertainty over trade and fiscal policies, which have generated volatility in financial markets and eroded consumer confidence.

“"A fixed-rate mortgage is essentially a hedge against inflation" — Hannah Jones, Realtor.com senior economic research analyst”

Historical Context

To understand the magnitude of this confidence crisis, it's useful to look back. During the housing bubble of the mid-2000s, homeownership peaked at 69.2% in 2004, fueled by easy credit and low rates. After the 2008 financial crisis, the homeownership rate fell to 62.9% in 2016, and has since recovered slowly to around 65.5% in 2025, according to U.S. Census Bureau data. However, access to housing remains unequal: Millennials and Gen Z face record prices and student debt, while Baby Boomers hold a disproportionate share of housing wealth.

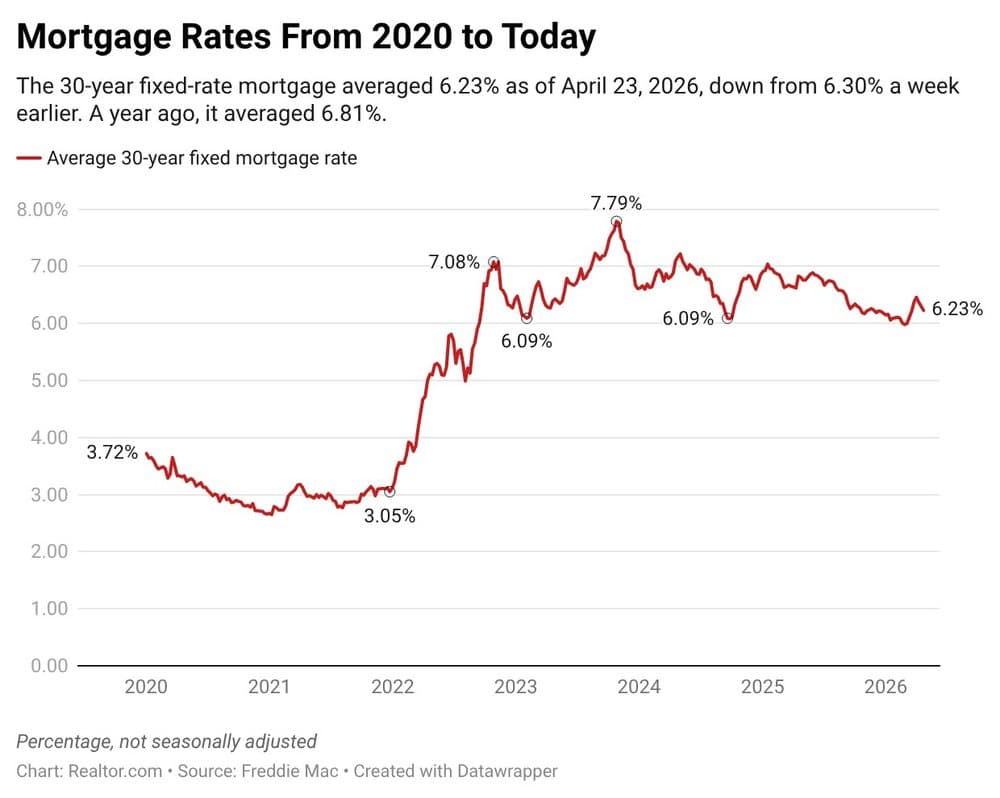

The COVID-19 pandemic exacerbated these trends. Mortgage rates fell to historic lows below 3% in 2020-2021, triggering a wave of purchases and refinancings. But pent-up demand, combined with supply chain disruptions and labor shortages, sent home prices soaring more than 40% between 2020 and 2022. Since then, the Federal Reserve has raised interest rates to combat inflation, pushing mortgage rates above 6%, which has cooled the market but not corrected prices.

By the Numbers

- Financial insecurity: 78% of Americans feel their financial future is not secure.

- American dream deferred: 72% believe they will never have enough money to achieve it.

- Savings sacrificed: 37% have given up long-term savings to prioritize short-term spending.

- Struggling for basics: 21% find it hard to afford rent/mortgage, food, and utilities.

- Opportunity cost: A $400,000 home appreciating at 3% annually costs $45,000 more in three years.

- Homeownership rate: 65.5% in 2025, still below the peak of 69.2% in 2004.

- Average mortgage rate: 6.3% for a 30-year fixed-rate mortgage in April 2026.

Why It Matters

The study reveals a paradox: 70% of respondents believe they've made smart financial decisions, yet 68% say a positive financial standing on paper doesn't guarantee future security. People feel they're playing by the rules, but the rules keep changing. This disconnect between perception and reality is concerning because it can lead to financial paralysis: if people don't trust that their efforts will pay off, they may stop saving, investing, or planning for the long term.

In this environment, homeownership stands out as an anchor. A 30-year fixed-rate mortgage at 6.3% on a median-priced $415,000 home with 20% down yields a monthly payment of $2,055—locked in for three decades. A renter paying $2,055 today could face $2,623 by 2031 if rents rise 5% annually. And every rent dollar is gone; every mortgage dollar builds equity. Additionally, homeownership offers tax benefits, such as mortgage interest deductions, which can reduce the tax burden.

But the barrier is real: prices and rates are high. Waiting for a better entry point risks being outpaced by appreciation. As Jones notes, home prices have risen in all but a handful of years over the past half-century. A $400,000 home appreciating 3% annually will cost $45,000 more in three years—often more than the down payment saved by waiting. A market correction like 2008 is unlikely given structural supply shortages. According to the National Association of Realtors, housing inventory remains at historically low levels, with only 3.5 months of supply in March 2026, well below the 6-month equilibrium.

Implications for the Economy

The lack of financial confidence has broader consequences. If consumers reduce spending and increase precautionary saving, economic growth could slow. Consumption accounts for roughly two-thirds of U.S. GDP, so a shift in consumer sentiment can have a significant impact. Moreover, low confidence can affect the labor market, as less secure workers may be less likely to change jobs or demand raises, which in turn can dampen wage growth.

In the housing sector, the combination of high unmet demand and limited supply keeps prices elevated, but affordability remains a problem. First-time buyers, in particular, are being priced out. According to a National Association of Realtors report, the median age of first-time homebuyers has risen to 36 in 2025, up from 33 in 2020, reflecting the difficulties of entering the market.

What This Means For You

For potential buyers, the decision isn't binary. There are nuances and strategies that can make purchase viable even in this environment.

- 1Run the real numbers. Factor in taxes, insurance, and maintenance (1-2% of home value annually). If the total is under 30% of your income, the purchase is sustainable. Use online calculators to simulate different rate and term scenarios.

- 2Explore assistance programs. Many states and cities offer down payment assistance or tax credits for first-time buyers. Don't rule out homeownership without checking. For example, the Federal Housing Administration (FHA) offers loans with as little as 3.5% down, and the Department of Agriculture (USDA) has zero-down loans for rural areas.

- 3Don't try to time the market. If you find a home you love and can afford it, the time may be now—especially if you plan to stay for at least 5-7 years. History shows prices tend to rise over the long term, and waiting can cost more than the wait.

- 4Consider alternatives to traditional buying. For instance, co-ownership models or adjustable-rate mortgages (ARMs) can offer lower initial payments, though they carry risks. You can also explore buying a smaller property or in a less expensive area.

What To Watch Next

The next few months will bring key signals. The Federal Reserve has signaled rates could stay high until inflation eases. A rate cut would lower mortgage costs but could also reignite demand and push prices up. The labor market will also be crucial: if unemployment rises, the Fed might cut rates to stimulate the economy, benefiting buyers.

On the geopolitical front, the Iran conflict remains unpredictable. A spike in oil prices could reignite inflation and delay any rate relief. Conversely, de-escalation could lower gas prices and ease pressure on buyers. Additionally, the midterm elections in November 2026 could bring changes in fiscal and regulatory policies that affect the housing market.

Long-Term Outlook

Despite current challenges, homeownership remains one of the most effective ways to build long-term wealth. According to the Federal Reserve, the median net worth of homeowners is $255,000, compared to just $6,300 for renters. This gap has widened over the past few decades and is likely to continue as home prices trend upward.

However, the current confidence crisis suggests many Americans are losing faith in the system. To restore confidence, policies addressing housing affordability, economic stability, and job security will be needed. In the meantime, buyers should be strategic and realistic, not letting fear freeze their financial decisions.

The Bottom Line

Financial security is elusive for most Americans, and homeownership isn't a panacea. But in an environment of persistent inflation and rising rents, a fixed-rate mortgage offers certainty that renting cannot match. Those who can make the leap will find not just a roof but a long-term asset. The key is to run realistic numbers and not let fear freeze the decision. For investors, the current market offers opportunities in the rental sector and REITs, but caution is warranted given the high-rate environment.